One of the important responses and mitigation tools for proper planning and resource allocation during a time of crisis is a budget. Kenya has experienced infestation of desert locusts, floods as well as the rise in confirmed COVID19 cases. Following the government-imposed restrictions to reduce the spread of the coronavirus, the country is currently not only undergoing a health crisis but also economic crisis.

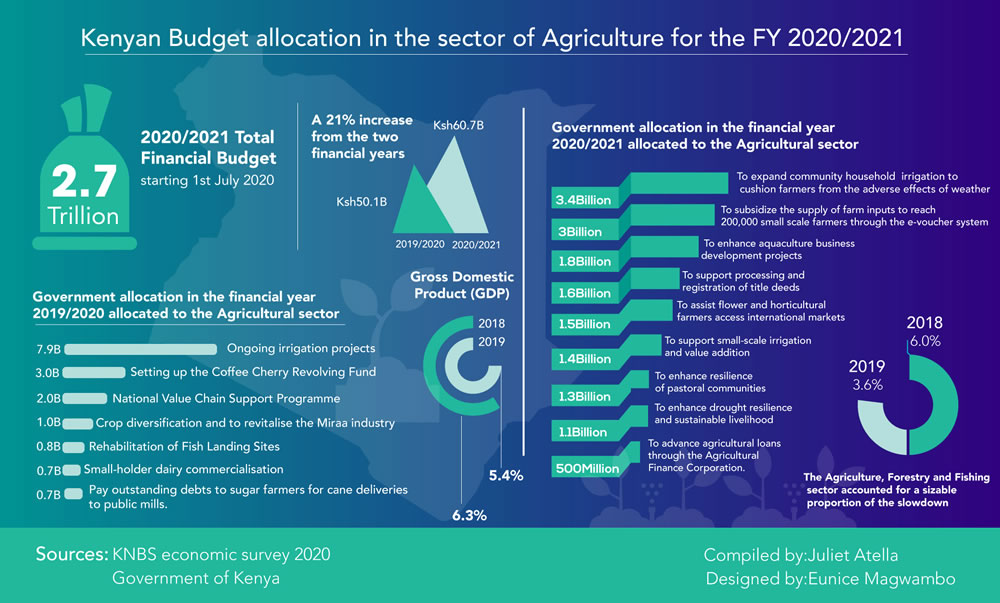

On 11th June 2020, the Cabinet Secretary for the National Treasury and Planning Ukur Yatani tabled a Ksh. 2.7 Trillion budget for the financial year 2020/2021 starting 1st July 2020. This comes against the backdrop of multiple the crises the country is undergoing.

One of the big four agenda of the government is to enhance food security for Kenyans. Under the sector of Agriculture and food security, the government has allocated Ksh. 8 billion to projects such as Kenya Climate Smart Agricultural Project, National Agricultural and Rural Inclusivity Project, Kenya Cereal Enhancement Programme, irrigation and land reclamation among others.

Additional allocation made by the government in the Agriculture and Food sector include: Ksh 3 billion to subsidize the supply of farm inputs to reach 200,000 small scale farmers through the e-voucher system; Ksh 3.4 billion for expanded community household irrigation to cushion farmers from the adverse effects of weather and further secure food supply chains; Ksh 1.5 billion to assist flower and horticultural farmers access international markets; Ksh 1.8 billion to enhance aquaculture business development projects; Ksh 1.4 billion to support small-scale irrigation and value addition; Ksh 1.3 billion to enhance resilience of pastoral communities; Ksh 1.1 billion to enhance drought resilience and sustainable livelihood; Ksh 1.6 billion to support processing and registration of title deeds; and Ksh 500 million to advance agricultural loans through the Agricultural Finance Corporation.

The budget allocation for the Agriculture and Food sector is an increase of 21 percent from Ksh 50.1 billion allocated in the 2019/2020 financial year to Ksh 60.7 billion allocated in 2020/2021.

As compared to the previous financial year 2019/2020, the government had allocated the funds to the following Agricultural sectors: Ksh 1.0 billion for crop diversification and to revitalize the Miraa industry; Ksh 0.8 billion for the rehabilitation of Fish Landing Sites; Ksh 0.7 billion for small-holder dairy commercialization. Ksh 7.9 billion for ongoing irrigation projects. Ksh 2.0 billion for the National Value Chain Support Programme ; Ksh 3.0 billion for setting up the Coffee Cherry Revolving Fund which was aimed at implementing prioritized reforms in the coffee sub-sector and Ksh 0.7 billion to pay outstanding debts to sugar farmers for cane deliveries to public mills. 2nd July 2020, Agriculture Cabinet Secretary Peter Munya announced sugar reforms and government directives on the importation of sugar and cane trading license. Other reforms include leasing of state-owned sugar mills to private investors for a period of 20 days to process and develop cane on farms such as Muhoroni, Chemelil, Sony, Nzoia and Miwani owned by the millers.

Programme based budget for FY 2020/2021, the State Department for Crop Development and Agricultural Research which is a merger of the former State Department for Crop Development and State Department for Agricultural Research, tabled a total expenditure for the FY 2020/2021 Ksh. 40.1 billion. The department is mandated to ensure sustainable development of agriculture for food and nutritional security and socioeconomic development. Improve the livelihoods of Kenyans by ensuring food and nutrition security through creation of an enabling environment, increased crop production, research and development, market access and sustainable natural resource management.

The report states that, “ Other key outputs to be delivered will include: subsidy of 582,500 metric tonnes (MT) of fertilizer; procurement and distribution of 750 tractors to farmers; identification, testing and up-scaling of 30 appropriate technologies by the Agricultural Technology Development Centres; increased maize productivity from 40 million bags to 67 million bags through expansion of acreage under maize production; increased ware potato productivity from 1.2 million MT to 1.6 million MT through increased certified seed production and distribution; increased rice productivity from 112,800 MT per acre to 271,000 MT through increased area under cultivation and subsidized mechanization, use of certified seeds and water saving technologies.”

With the comprehensive reforms under the department of Agriculture, the programme based budget further adds, ” The State Department will also ensure increased cotton production from 40,000 MT to 100,000 MT; increased tea production from 1.1 million MT to 1.6 million MT; annual sugarcane production from 4.8 million MT to 8.5 million MT and increased pyrethrum production from 300 MT to 3,000 MT by 2022.”

According to the KNBS economic survey 2020, the real Gross Domestic Product (GDP) is estimated to have expanded by 5.4 per cent in 2019 compared to a growth of 6.3 per cent in 2018. The growth was spread across all sectors of the economy but was more pronounced in service-oriented sectors. The Agriculture, Forestry and Fishing sector accounted for a sizable proportion of the slowdown, from 6.0 percent growth in 2018 to 3.6 per cent in 2019.

Last year, the country experienced a mixed weather phenomenon. This was characterized by drought during the first half of the year, followed by high rainfall in the second half of the year. This culminated in reduced production of selected crops and pasture for livestock.

According to Timothy Njagi Njeru and Milton Were Ayieko from Tegemeo Institute of Agricultural Policy and Development, Egerton University on COVID-19 on Kenya’s food security, a key challenge for the country is to raise productivity in the agriculture sector. This would not only ensure food availability, but potentially lift households out of poverty. For the government to attain this, it must reduce reliance on rainfed agriculture systems, use modern varieties and technologies by enhancing investments in extension systems, build resilience of farmers against the effects of climate change and variability, and improve agricultural market systems and infrastructure. The 2019 population census states that, total agricultural land operated by households stood at 10.3 million hectares, equivalent to 17.5 per cent of the total land area in the country. Of the total enumerated households, 6.4 million were practicing agriculture. Households growing crops were 5.6 million while those practicing irrigation were 369,679. In total, 5.1 million households were engaged in maize cultivation followed by 3.6 million cultivating beans. Livestock keeping was practiced by 4.7 million households while aquaculture and fishing activities were practiced by 29,325 and 109,640 households, respectively.

With the current Covid-19 pandemic situation, nationally, 30.5 per cent of households were unable to pay rent on the agreed date with the landlord. 52.9 per cent stated their main reason unable to pay rent is due to reduced income/earnings. For households, which are going to be devastated by these economic realities, the government of Kenya needs to put in place adequate safety nets to assure food security and support food producers.

–

This article is part of The Elephant Food Edition Series done in collaboration with Route to Food Initiative (RTFI). Views expressed in the article are not necessarily those of the RTFI.